US Healthcare Out-of-Pocket Estimator

Estimate how much you will actually pay for a medical procedure based on your private insurance plan details.

Cost Breakdown

Key Takeaways

- Most healthcare providers in the US are private businesses, not government-run.

- Access is primarily managed through private health insurance plans.

- 'Cash pay' or 'direct primary care' are alternatives for those without insurance.

- Costs vary wildly based on the provider's negotiated rates with insurance companies.

- The system is fragmented, meaning you must check if a doctor is 'in-network'.

The Reality of the American System

To understand private healthcare in the US, you first have to throw away the idea of a national health service. In the US, Private Healthcare is a system where medical services are provided by private practitioners, clinics, and hospitals rather than the state. While the government does run programs like Medicare (for seniors) and Medicaid (for low-income individuals), the actual buildings and doctors are often still private entities that simply accept government payments.

If you're looking for "private care" because you want to avoid long queues, you've come to the right place. Wait times for specialists are generally much shorter than in the UK or Canada. However, the trade-off is the cost. You aren't just paying for the doctor's time; you're paying for the overhead of a massive corporate healthcare infrastructure.

How You Actually Access Care

You can't typically just walk into a specialized surgical center and ask for a price list. Most of the time, you'll access care through one of three main paths:

- Employer-Sponsored Insurance: This is the most common route. Your job pays a portion of your premium to a private insurance company, and you pay the rest. This gives you a defined "network" of doctors you can visit.

- The Individual Market: If you're a freelancer or unemployed, you buy a plan through the Health Insurance Marketplace (established by the Affordable Care Act). This is still private insurance, just purchased individually.

- Self-Pay (Cash Pay): Some people choose to skip insurance entirely. They pay the doctor directly for every visit. While this sounds simple, it can be incredibly expensive for anything more than a basic check-up.

Here is a quick look at how these options compare in terms of accessibility and cost.

| Method | Wait Times | Upfront Cost | Financial Risk |

|---|---|---|---|

| Employer Plan | Low to Medium | Moderate (Monthly) | Low (capped by out-of-pocket max) |

| Marketplace Plan | Low to Medium | Variable (Subsidy based) | Moderate |

| Cash Pay | Very Low | High per visit | Very High (no safety net) |

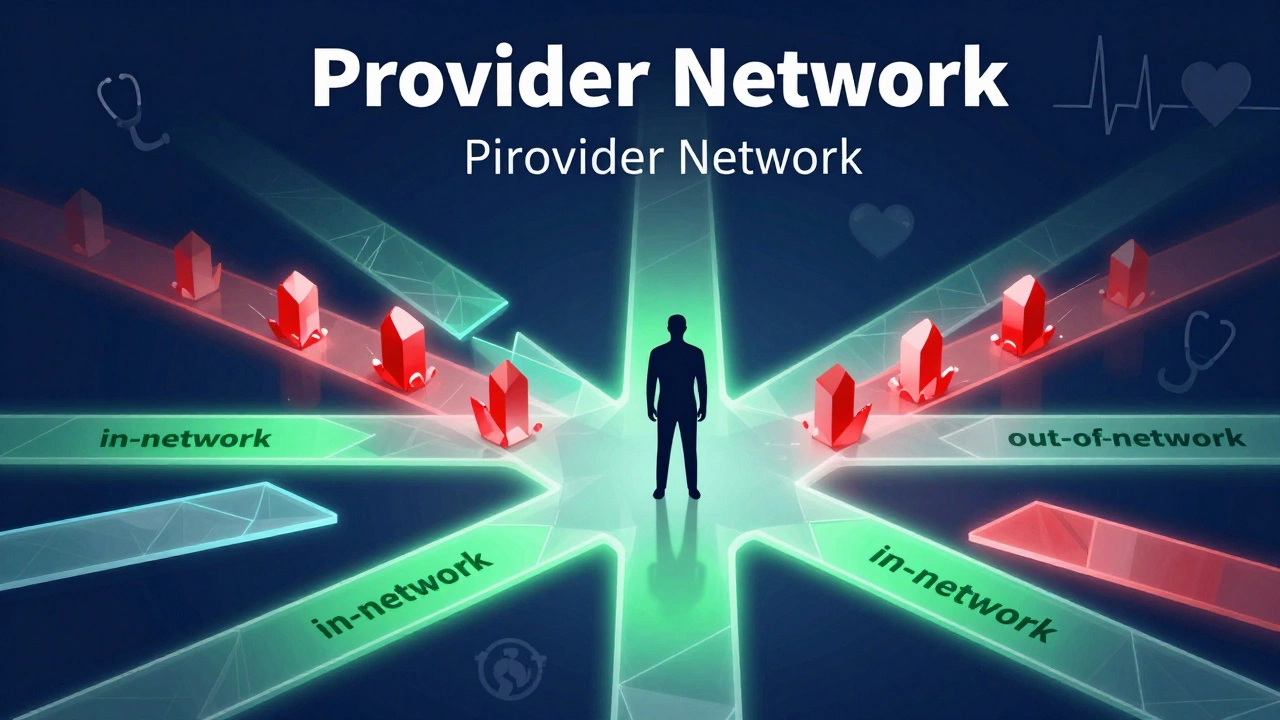

The Concept of the 'Network'

One of the most confusing parts of the US system is the Provider Network. A network is a list of doctors and hospitals that have signed a contract with your insurance company to provide services at a discounted rate. If you go to a doctor "in-network," your insurance covers a large chunk of the bill. If you go "out-of-network," the insurance company might refuse to pay anything at all, leaving you with a massive bill.

This creates a weird dynamic where you might have a world-class surgeon living three blocks away, but you can't see them because they don't accept your specific insurance plan. It's not that the doctor isn't "private"-they are-it's that they haven't agreed to the insurance company's pricing rules.

Direct Primary Care: A Modern Alternative

If you're tired of the insurance game, there's a growing trend called Direct Primary Care (DPC). In this model, you pay a monthly membership fee (like a gym membership) directly to your doctor. In exchange, you get unlimited office visits, direct access to your doctor's cell phone, and longer appointments.

DPC removes the middleman. The doctor doesn't have to spend hours filing paperwork for insurance companies, and you don't have to worry about co-pays. However, DPC only covers primary care. If you need a major surgery or an MRI, you'll still need traditional insurance or a huge amount of cash.

What Does It Actually Cost?

Pricing in the US is famously opaque. A single blood test might cost $50 at one clinic and $500 at another. This happens because hospitals negotiate different rates with different insurers. To navigate this, you have to look at three key numbers on your plan:

- Deductible: This is the amount you pay out of your own pocket before the insurance company starts paying a dime. If your deductible is $3,000, you pay for everything until you hit that mark.

- Co-payment (Co-pay): A flat fee you pay for a specific service. For example, $30 for a GP visit or $100 for an urgent care trip.

- Coinsurance: This is a percentage of the cost. If your coinsurance is 20%, you pay 20% of the bill and the insurance pays 80%.

For those without insurance, some clinics offer a "sliding scale" based on income, but this is usually found in community health centers rather than high-end private practices.

Avoiding Common Pitfalls

If you are navigating the US system for the first time, there are a few traps that can lead to financial disaster. First, always ask for a "good faith estimate" if you are paying cash. This is a legal requirement under the No Surprises Act, which protects patients from unexpected bills. It ensures that you know the approximate cost of a procedure before it happens.

Second, be careful with "Urgent Care" versus the "Emergency Room (ER)." An ER visit is the most expensive way to receive care. If you have a deep cut or a bad flu, an Urgent Care center is a private clinic that is significantly cheaper and faster than a full-scale hospital emergency department.

Can I just pay cash for a doctor's visit in the US?

Yes, you can. This is often called "self-pay." Many doctors offer a discount if you pay in full at the time of service because it saves them the hassle of billing an insurance company. However, this is only viable for routine visits; major procedures without insurance can cost tens of thousands of dollars.

Is there a difference between private and public healthcare in the US?

Unlike the UK's NHS, the US doesn't have a truly "public" healthcare system where the government owns the hospitals. Instead, it has public insurance (Medicare/Medicaid) that pays private providers. So, while the funding might be public, the delivery of care is almost always private.

What is an 'in-network' provider?

An in-network provider is a doctor or hospital that has a contract with your insurance company. They agree to accept a lower, pre-negotiated rate for their services. If you use an out-of-network provider, you may have to pay the full market price, as your insurance may not cover the difference.

How do I find a private doctor if I don't have insurance?

You can search for "Direct Primary Care" providers in your area or look for clinics that advertise "cash-pay" or "self-pay" options. Many specialized clinics also allow you to book appointments without insurance, provided you pay the fee upfront.

Does private healthcare in the US mean better quality?

The US has some of the most advanced medical technology and shortest wait times for specialists in the world. However, "better" is subjective. While the high-end private care is exceptional, the lack of universal access means that overall public health outcomes are often lower than in countries with integrated systems.

Next Steps and Troubleshooting

If you've just arrived in the US or are looking to switch your care, start by auditing your insurance policy. Look for the "Summary of Benefits and Coverage" document; this is the cheat sheet that tells you exactly what your deductible and co-pays are. If you find that your premiums are too high, check the government marketplace for subsidies that might lower your monthly cost.

For those who find the system overwhelming, consider using a patient advocate. These are professionals who help you negotiate medical bills and find the most cost-effective providers. If you receive a bill that seems impossibly high, don't pay it immediately. Ask for an "itemized bill" with CPT codes. Often, simply asking for a detailed breakdown causes hospitals to remove erroneous charges or "phantom' fees" that weren't actually performed.